Nature of the Data

The nature of RPA data is financial: the recorded flows are structured according to an economic classification consistent with the financial accounting criteria adopted in the preparation of public entities’ financial statements, thereby reconstructing a comprehensive framework of all transactions generating monetary movements.

With reference to the final accounts of entities, the RPA System prioritizes the recording of transactions on a cash basis; therefore, revenue and expenditure data are recorded at the time payments are effectively made and revenues are actually collected.

The breadth of the universe covered, the Extended Public Sector (EPS), requires consideration of both entities adopting financial accounting systems and those applying accrual-based (economic) accounting systems. This includes not only all public enterprises belonging to the Extra-PA sector, but also certain Public Administration entities, such as Local Health Authorities (LHA) and Chambers of Commerce.

This requires the application of a rigorous methodology to convert accrual-based (economic) accounts into financial accounting for all entities adopting such systems. For further details and in-depth information, reference should be made to the Guide to the Regional Public Accounts ,the 2022 updates,and the latest methodological innovations introduced in 2023.

The economic categories adopted by the RPA System have been defined with the aim of ensuring comparability among entities within the same universe, in the absence of a uniform classification applicable to all public entities within the Extended Public Sector (EPS), and of improving comparability with other public finance aggregates.

In particular:

capital expenditure net of financial transactions: includes capital expenditure excluding the categories “Acquisition of equity holdings and capital contributions” and “Granting of loans, etc.”;

development-related expenditure: includes capital expenditure net of financial transactions and current expenditure for vocational training;

investments: refers to the sum of the categories “Acquisition and construction of real estate and public works,” “Acquisition and construction of other tangible and intangible fixed assets,” and “Acquisition of financial assets.”

The economic categories adopted by the RPA System are summarized in the table below Revenue and Expenditure Categories.

The Regional Public Accounts adopt, with reference to expenditure, a sectoral classification aligned with that used in Public Accounting and particularly useful for evaluating spending. The same does not apply, however, to the classification of revenue flows, most of which are not originally linked to specific sectors of intervention.

The 29 category sectoral classification adopted by the RPA represents the minimum level of detail at which data are available. Depending on specific uses, the data can be re-aggregated according to different criteria. By using the mapping schemes between RPA sectors and the aggregations adopted in regional monographs, it is also possible to derive a 10 category sectoral breakdown.

In the Regional Public Accounts System, each entity is treated as a provider of final expenditure through the elimination of transfer flows between entities belonging to the same level of government. A consolidation process is therefore carried out, allowing the determination of the total expenditure actually disbursed within the territory or revenues effectively collected, without the risk of duplication.

Consolidation is directly dependent on the reference universe, and changes in the universe affect both consolidated figures and the final results. Consequently, when only Public Administration (PA) is considered, transfers to National Public Enterprises (NPE), Regional Public Enterprises (RPE), and Local Public Enterprises (LPE) are not eliminated, as these entities fall outside the PA. However, when the Extended Public Sector (EPS) is considered, transfers to NPE, RPE, and LPE are eliminated to avoid double counting.

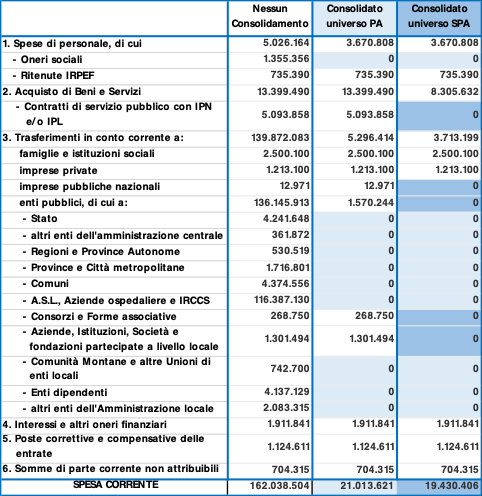

The following example, illustrating different levels of consolidation for current expenditure across the various universes, helps to clarify the concept.

The geographic reference universe for the RPA consists of the 19 Italian Regions and the 2 Autonomous Provinces of Trento and Bolzano. Each territorial unit is coded according to the ISTAT standards to facilitate consultation and ensure comparability with other databases. The territorial aggregates commonly used refer to the five ISTAT macro-areas:

North-West: Piedmont, Aosta Valley, Lombardy, Liguria;

Nord-East: Autonomous Province of Trento, Autonomous Province of Bolzano, Veneto, Friuli-Venezia Giulia, Emilia-Romagna;

Centre: Tuscany, Umbria, Marche, Lazio;

South: Abruzzo, Molise, Campania, Apulia, Basilicata, Calabria;

Islands: Sicily, Sardinia.